Retainer compression on social and content is real. US marketing agencies that add AI video production as a service line are turning it into the highest margin work on their books.

The retainer that funded a mid sized US social media agency in 2022 does not fund the same agency in 2026. Meta’s Advantage+ has moved a meaningful share of creative optimization inside the ad platform. TikTok Symphony does the same on the other end. Content marketing retainers are absorbing pressure from AI Overviews, which now sit above 40% of informational queries and cut through the organic click stream that most content strategies target for traffic. The Adweek editorial from March 2026 said what agency owners already knew. The pricing model is eroding.

The strategic question for owners of US content, social, and creative agencies is what to sell next. The answer that most operator conversations converge on right now is AI video production. The reason sits in the P&L. The gap between production COGS and market sell price for finished video has widened faster than for any other service line an agency can add this year.

This is the margin case, laid out cleanly.

Why the existing service lines are compressing

Three forces are pressing on the two service lines that most US marketing agencies still rely on for the majority of their retainer revenue.

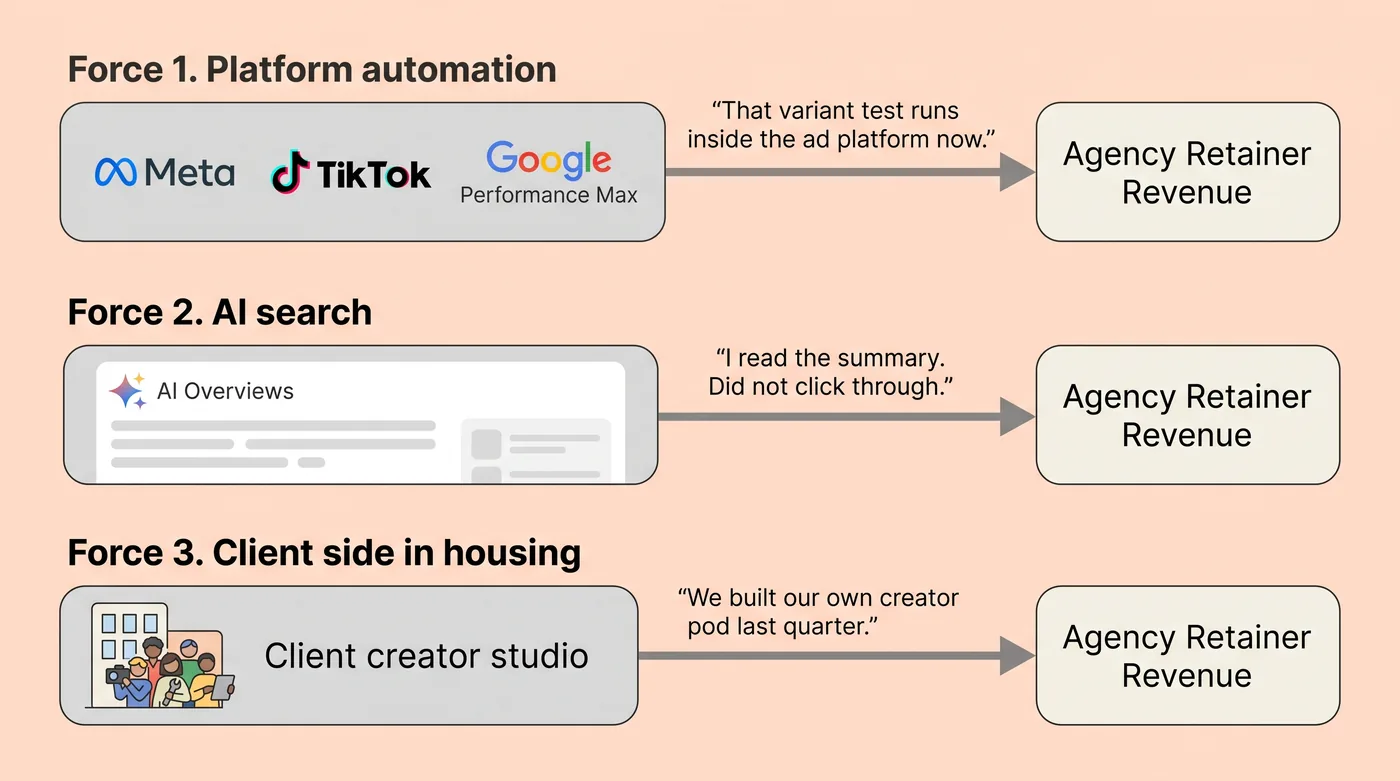

Fig 1 – The three forces compressing social and content agency retainers in 2026.

Platform automation. Meta Advantage+ campaigns now handle the bulk of automated creative variation for advertisers who opt in. Google’s Performance Max does similar work for search and display. TikTok Symphony generates ad script and visual variants inside the platform. Every hour of creative optimization that moves inside the ad platform is an hour the agency used to bill for.

AI search. AI Overviews now sit above 40% of informational queries and cut through the organic click stream that most content strategies target for traffic. Clients who used to pay 4,000 dollars a month for a content calendar are now asking why the deliverable count has not tripled. The margin on written content has moved down and to the right on almost every agency rate card visible in 2026.

Client side in housing. Enterprise clients with 20 million dollars or more in annual marketing spend increasingly run a creator studio, a paid media pod, and a content operation inside their own building. Commerce media spend is on track to overtake TV in 2026. That signals where budgets are moving, and where they are moving is toward outcomes the historical service lines were not built to price against.

An agency owner sitting inside this compression has three choices.

- Cut headcount and defend margin at a smaller scale.

- Chase specialization inside the existing service line and try to hold rate.

- Add a service line that carries fundamentally different economics.

The first two are defensive at best. Cutting is a one time gain. Specialization protects for 12 to 18 months before the platform absorbs the specialization. The third choice is the only one that changes the shape of the P&L.

AI video production is the version of that third choice that is available right now, priced right, and structurally underdeveloped inside most agency organizations. That is what makes it the diversification play of 2026.

Why AI video is different from the other AI services agencies could add

Two structural facts about AI video production distinguish it from the other services an agency could theoretically productize this year.

The first fact is the demand curve. The IAB’s 2026 Digital Video Ad Spend and Strategy report projected US digital video ad spend to surpass 80 billion dollars this year, growing at roughly 13% versus 11% for CTV, with social video outpacing CTV for the first time. Short form video creative is the constraint every client on paid social is trying to solve for. The demand for variants, hooks, and platform native cuts is measured in hundreds per month for any brand running a real testing program.

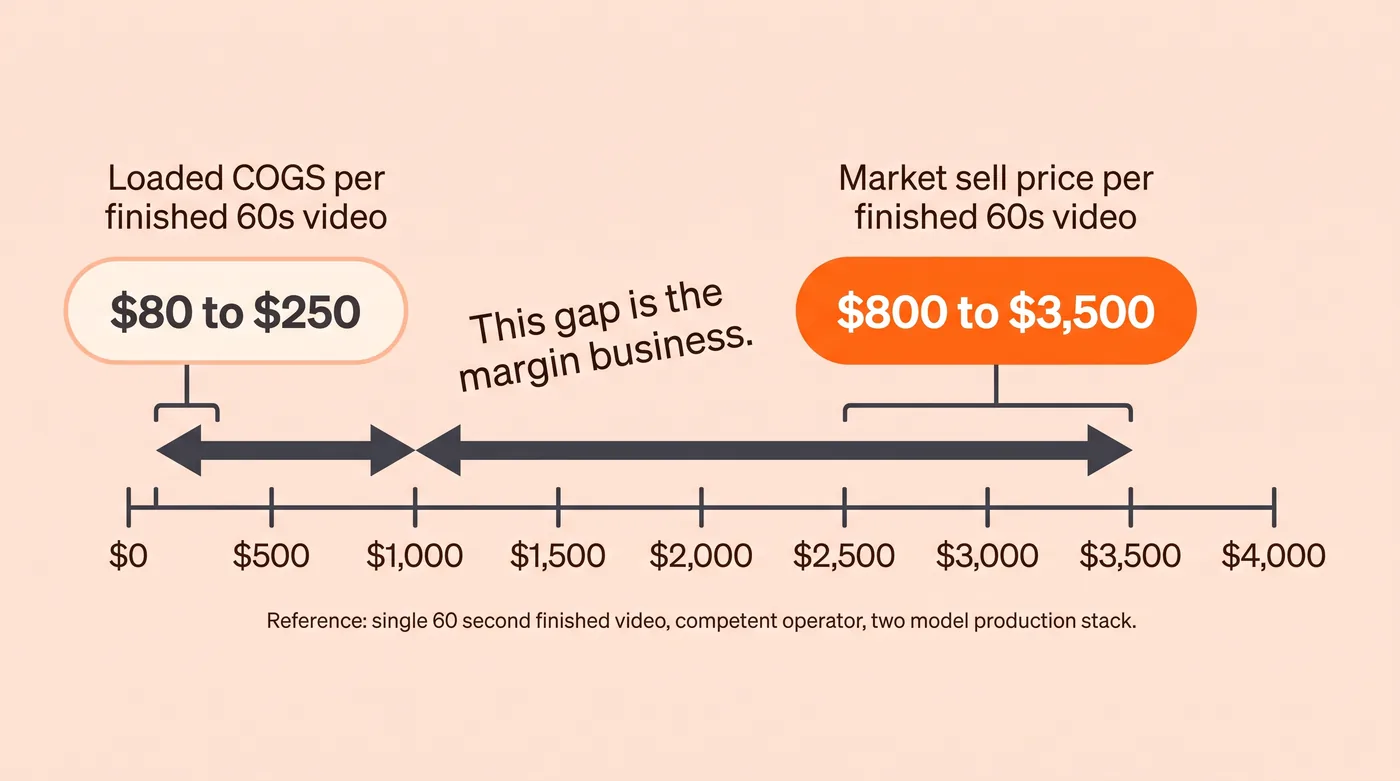

The second fact is the sell price gap. Current published pricing on frontier video models puts high fidelity generation at roughly 0.50 dollars per second of output with audio, and faster preview tiers at half that rate. A 60 second finished video assembled from those generations, with editorial, sound design, and captioning added on top, carries a loaded COGS of somewhere between 80 and 250 dollars depending on model mix and revision count. The market sell price for the same finished asset sits between 800 and 3,500 dollars.

That gap is what makes AI video production a margin business.

Fig 2 – Loaded COGS versus market sell price for a single 60 second finished video, competent operator, two model production stack.

The comparison worth drawing is with AI written content, where clients already know the raw model cost per word and price accordingly. The knowledge gap around AI written content has closed. The knowledge gap around AI video has not, because the reference price in the client’s head is still anchored to the 5,000 dollar shoot they paid for in 2023. That anchor is not going to hold for another 24 months. Agencies that build the service line now capture the premium during the reprice window and hold retention through the compression that follows.

The economics of moving early are what most existing coverage misses. This is an 18 month margin window, not a permanent one.

Three ways to structure the offer, and the P&L difference between them

There are three ways US agencies are currently structuring AI video production inside their service menu, and the choice matters more than the tool selection.

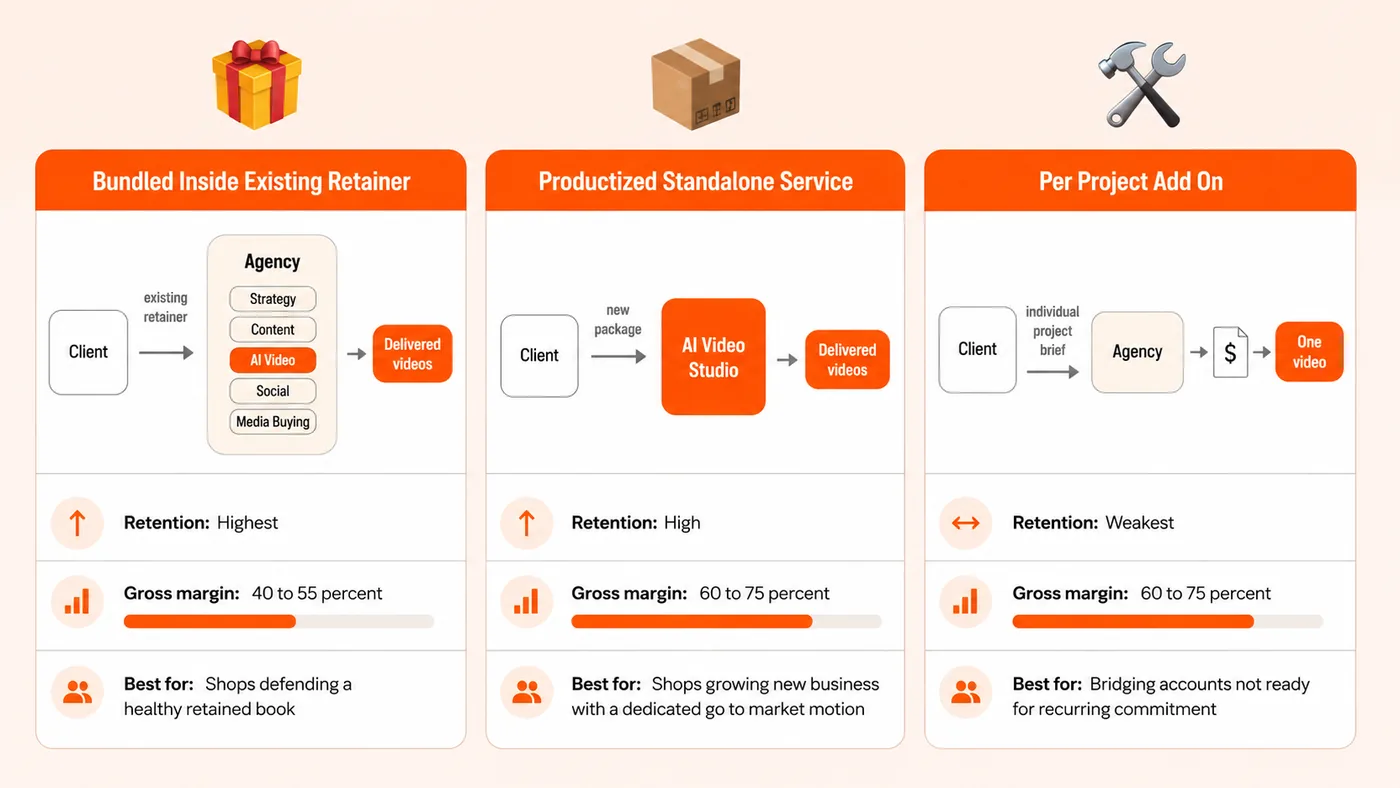

Fig 3 – Three service line structures with retention, margin, and best fit at a glance.

Bundled inside an existing retainer. The agency adds 8 to 15 short form video assets per month to a paid social or content retainer that already exists, without adjusting the top line. This is the highest retention path because the client sees additional deliverables at the same rate. It is also the lowest margin path in absolute terms because the agency absorbs the COGS without repricing. The P&L works because retention on video inclusive retainers runs 20 to 30% higher than on retainers without video, and lifetime value more than compensates. This is the play for shops that already have a healthy book and want to defend it.

Productized standalone service. The agency builds a dedicated AI video production offer with named packages, deliverable counts, and revision policy, and sells it as its own line. Pricing typically sits between 3,500 and 15,000 dollars a month for structured packages covering 20 to 80 finished videos. This is the highest margin path and the one that shows up cleanly in the financials as a new service line. It requires more upfront investment in offer design, sales collateral, and operational build. This is the play for shops that want to grow the business and are willing to run a dedicated go to market motion around it.

Per project add on. The agency invoices AI video production on top of existing scope, per deliverable or per campaign. Margins per project are strong, often between 60 and 75% gross. Retention is the weakest of the three because there is no recurring commitment. The financial trajectory shows up cleanly in the P&Ls of shops that have made this shift. A US content agency in the 15 person range that ran the full transition through 2025 into 2026 cut per video pricing by 30%, cut COGS by 86%, and moved overall profit margin from 18% to 31% inside 12 months. Revenue from video services grew more than 3x. The shape is repeatable.

The three structures are not mutually exclusive. Most shops that get this right end up running the bundled play for their retained accounts and the productized play for new business, with per project available as a bridge for accounts not ready to commit.

What the canonical deliverables actually cost to produce

Loaded COGS ranges below assume a two model production stack (a primary generation model plus an editorial pass), a 10 to 15% revision buffer, and internal creative time priced at 65 dollars per hour blended.

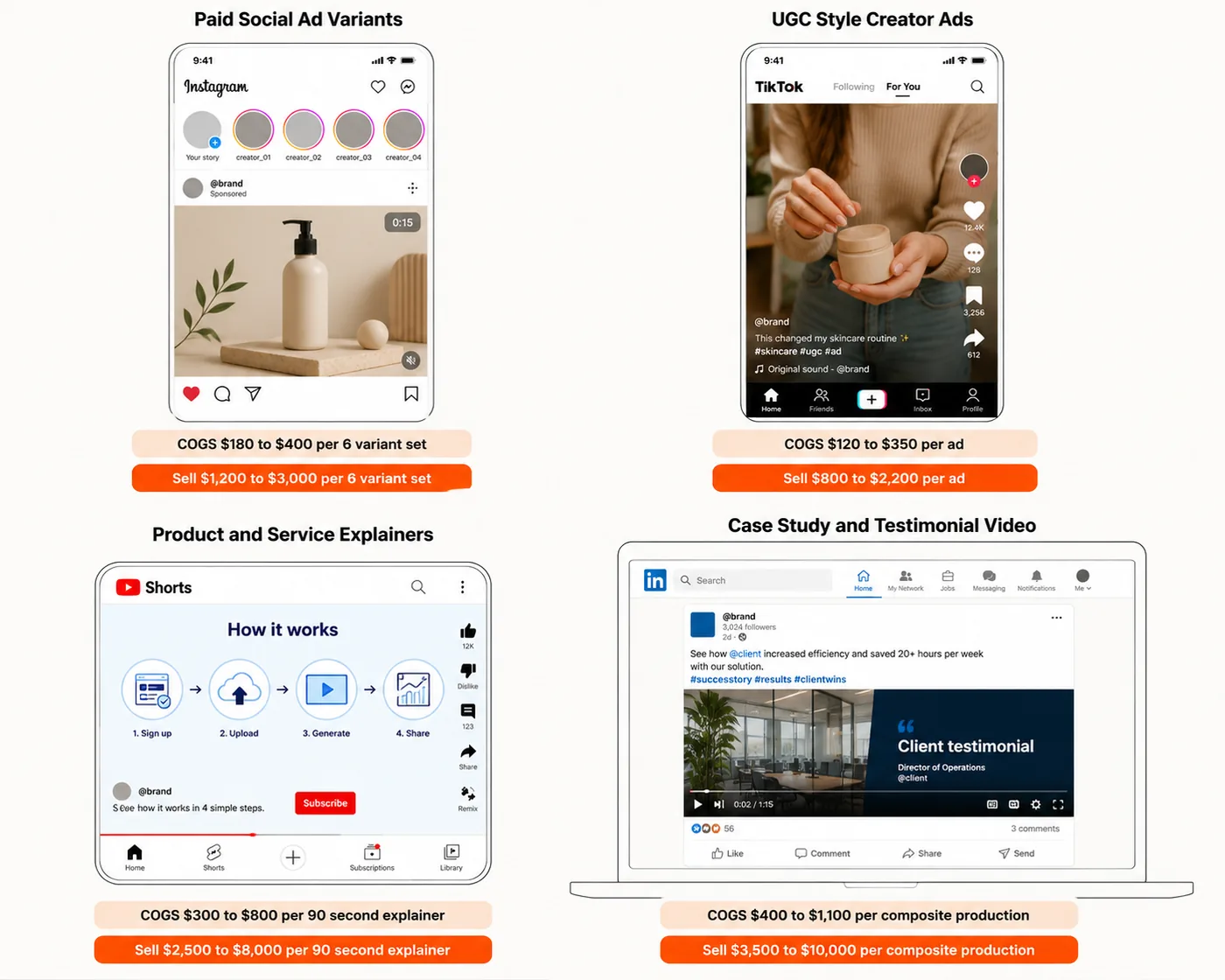

Fig 4 – The four canonical AI video deliverables in the platform surfaces where they run, with COGS and sell price bands per unit.

Paid social ad variants. A set of 6 platform native variants (Meta, TikTok, YouTube Shorts) built from one script, one hook family, and three visual treatments. Loaded COGS runs 180 to 400 dollars per variant set. Market sell price sits between 1,200 and 3,000 dollars. Highest volume deliverable and the most common entry point.

UGC style creator ads. A single 30 to 60 second creator style ad built with a licensed AI actor library or generated avatar. Loaded COGS runs 120 to 350 dollars per ad. Market sell price sits between 800 and 2,200 dollars. Performance parity with real UGC is now the benchmark, and current model quality clears it in most B2C categories.

Product or service explainers. A 60 to 120 second explainer combining generated footage, motion graphics, and voiceover. Loaded COGS runs 300 to 800 dollars. Market sell price sits between 2,500 and 8,000 dollars. Highest ratio of sell price to COGS in the deliverable stack.

Case study and testimonial video. A composite production combining real client footage or interview audio with generated B roll, graphics, and platform cuts. Loaded COGS runs 400 to 1,100 dollars. Market sell price sits between 3,500 and 10,000 dollars. Best fit for B2B agencies with SaaS or enterprise clients.

The ranges assume competent operators. Shops that have not built a repeatable production runbook see COGS 40 to 80% higher, mostly from revision drag and model swap tax. This is the operational cost that most agencies underestimate when they run the business case.

The service design questions most agencies get wrong

The failure mode for AI video production as an agency service line sits in the service design around the model output. Model quality is rarely the issue.

Usage rights and IP ownership. Client contracts need to specify who owns the finished asset, what happens to underlying prompts and generation seeds, and what license the client has to reuse or resell the output. Most agencies default to a work for hire structure. That is usually correct. Getting it wrong once creates a legal exposure that erases the margin from the first 40 clients.

Disclosure. Meta and TikTok both enforce AI content disclosure requirements in 2026 for photorealistic or realistic sounding output. Agencies that ship at scale bake disclosure into the delivery process. Leaving it to the client creates compliance debt that compounds across campaigns. Some tool stacks flag output automatically. Others do not. The service design has to account for the difference.

Revision policy. This is where the margin dies. A three revision cap on paid social variants and a two revision cap on hero deliverables holds the P&L. Unlimited revisions turn a 70% gross margin deliverable into a 30% one within two campaigns. Every agency that ships AI video at real volume learns this the hard way. The ones that build the cap into the SOW from day one skip the learning cost.

Turnaround SLA. A 48 hour turnaround is the current market expectation for paid social variants. Delivery at that speed is table stakes. Shops still selling 5 to 7 day turnaround on variant work are losing accounts to shops that can hit 48.

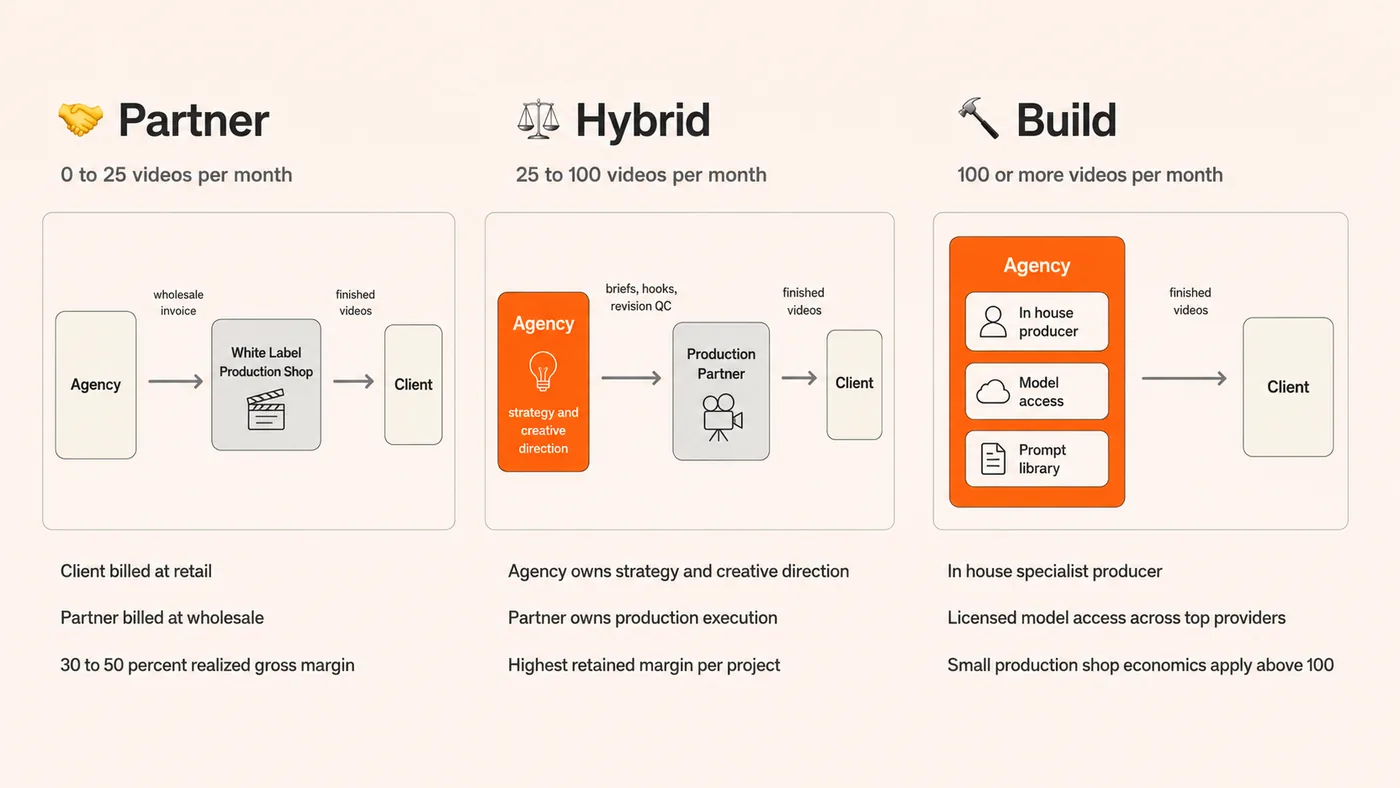

Build, partner, or hybrid

The operator decision underneath all of this is whether to build the capability in house, partner with a white label production shop, or run a hybrid.

Building in house works at real volume. Hiring one specialist producer, licensing model access across the top three or four providers, and running a shared prompt library gets an agency to 30 to 60 finished videos a month with acceptable margins. Below that volume the fixed cost of the specialist salary drags returns. Above 100 videos a month, the agency needs two producers and starts to look like a small production shop.

Partnering with a white label production shop makes sense at low volume and during the learning window. The agency invoices the client at retail, invoices the partner at wholesale, and keeps the difference. Realized gross margins after payment processing, revision buffer, and account management overhead run 30 to 50% for competent operators. This is a real business, and it takes management.

The hybrid works best for shops that want to own the client relationship and creative direction while offloading production execution. The agency handles script, brief, hook development, and revision QC. The partner handles generation, editorial, and delivery. This structure retains the highest margin while keeping the fixed cost line clean.

The right answer is volume dependent.

- Below 25 videos a month, partner.

- Between 25 and 100, hybrid.

- Above 100, build.

Fig 5 – The build, partner, and hybrid decision mapped to monthly video volume.

What this looks like 18 months from now

Two forces will collapse the current margin window.

Real time generation is the first. Nvidia’s April 2026 announcement with Runway showed generation moving toward interactive speed, with model output updating as prompts change. When that ships broadly, the iteration cost of every variant collapses further and the reference price in the client’s head starts to move. The 3,000 dollar variant set becomes a 1,200 dollar variant set within four quarters of general availability.

Client sophistication is the second. Every client marketing team that hires an AI native associate this year will know what a Veo generation costs by the end of the year. That knowledge transfers to procurement inside 6 months. The information asymmetry that funds the current margin sits on a shorter timeline than most agency owners assume.

The implication is straightforward. Agencies that add AI video production as a structured service line this year capture the reprice window and lock retention through video inclusive retainers before the market prices in. Agencies that wait until 2027 add a commoditized service line into a commoditized rate card. The margin structure is the same as any other technology adoption curve. Early is the strategy.

Closing

The strategic case for adding AI video production as a service line in 2026 sits in the shape of the P&L on the other side of the current retainer compression. The service line clears 60 to 75% gross for competent operators, retains stronger than the base retainer it attaches to, and prices at a premium that will not survive the next 18 months. The move is available. The window is finite.

Add AI Video Production to your agency service menu

Clixlogix builds AI video production programs for US marketing, social, and content agencies. Offer design, delivery pipeline, and white label execution at agency scale.

Explore AI Video Production Services